These last few weeks, investor attention has shifted away from all-things AI to the latest conflict in the Middle East. But when the clash ends, sooner rather than later we hope, AI will once again take center stage and for good reason. This rapidly evolving technology has the capacity to fundamentally alter key aspects of the real economy and, by extension, financial markets.

In our October newsletter, we wrote about the structure of the AI marketplace, focusing mostly on the major players and the services they provide (this would be a good starting point for those not as steeped in the world of AI). Now, with that work as background, we turn to the big question on investors’ minds today. What is the business case supporting AI use? More specifically, who is using the technology, and, importantly, who is willing to pay for it?

Answering these questions is no easy task for at least two reasons. First, the business models of most AI firms, and the underlying technology, are rapidly evolving. Second, because many of the major players remain privately held, access to critical information is limited. Nonetheless, let us look at what we do know.

So, who are all these companies using AI? While “use cases” are rapidly expanding, the clear winners in the AI deployment race today are software developers who use it to generate code and test software, as well as customer service functions (think chatbots, automated email responses, and call center assistants). Marketing and sales teams are also using AI to personalize advertising, automate ad copy writing, and design targeted ad campaigns. These deployments all have several things in common; they involve rules-based, repetitive tasks that rely on large, stable data sets—a feature of all types of language, including code. Importantly, in each of these cases, easily measured and robust financial benefits (read: cost savings) have also spurred adoption.

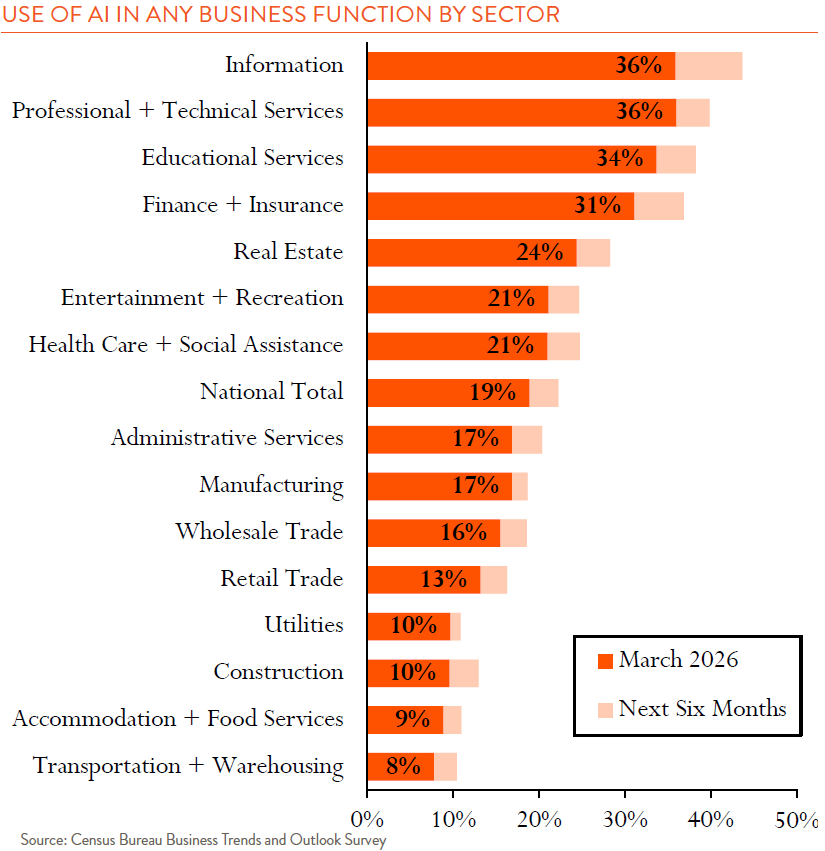

The chart below provides further details on the types of firms that are using AI today for any business purpose. Not surprisingly, the technology sector ranks highly as do a range of other “knowledge-based” industries such as legal, engineering, education, and finance. Meanwhile, many “old economy” sectors, such as construction and manufacturing, and customer facing areas, like retail and food services, lag.

When compared to historical technological innovations, the current rate of AI adoption has been lightning-fast. Consider the case of electricity, which first became available for commercial use in the U.S. in the early 1880s. By 1909, electricity still provided only 9% of manufacturing horsepower and it would take another 20 years for it to provide more than 50%. In a more recent example, it took a full 13 years for work use of computers to double from approximately 25% in 1984 to 50% in 1997. From the second chart (below), we can see that at a national aggregate level, AI is already used by an estimated 15% of businesses in producing goods and services and by around 20% in any business function (the big jump is when the Census Bureau changed the question’s wording). Other surveys of AI use have found that only 8%-13% of workers use it on a daily basis.

And yet, from the headlines we read, we might assume these numbers are higher. Despite AI’s early success and transformative potential, it is important to keep in mind that for many firms, obstacles to adoption remain formidable. In the business context, the technology often involves manipulating enormous amounts of critical, non-public information. Clearly understanding and mitigating the related privacy, security and regulatory risks of this work is both complicated and time consuming. For example, in monitoring the companies among our investment holdings, we find that many firms, especially those in non-tech sectors, are approaching AI adoption carefully, focusing first on using the technology to achieve internal productivity-related goals before embarking on more customer-facing initiatives.

This measured approach may be contributing to the technology’s still limited impact on the nation’s productivity measures. Non-farm business sector productivity gained 2.1% in 2025, above the 1.8% average experienced over the prior ten years but roughly in line with the long-run 2.2%. In a recent article, The Economist points out that further adoption alone will not spur productivity growth. AI’s impact, instead, will only appear once firms figure out how to reorganize their business models around it (and train staff to use it). This will be a trial and error, iterative process that is likely to be measured in years, not months.

And productivity gains are not going to be uniform across sectors. Presumably, companies adopting it more rapidly, such as software development, already see a clearer business case than, say, food services. Which brings us to the “who is willing to pay” for it question.

What these AI model companies charge for use has evolved according to the well-worn tech company playbook: charge nothing for your product up front, build your user base, and then once the technology becomes widely embraced, charge a fee. Open-AI first released ChatGPT to the public back in November of 2022, and while it still offers a free version, the company started charging $20/month in February of 2023 for its cutting-edge models. AI-related products, and their fee structures, have rapidly evolved since then.

While most individual users continue to pay low, monthly fees, “enterprise” or business users with more robust needs are now paying for model “use” which is measured by the number of “tokens” processed or seconds of compute time used. Payment plans may also be structured as agreements with cloud platform providers, like Microsoft or Google, that provide dedicated infrastructure and a certain level of processing power.

This enterprise use case and paying for compute is where the real money is made. While some might balk at a non-subscription payment model, as the return on AI investment becomes more proven, we expect willingness to pay to rise as well. Consider a software development function where an AI model can code better and faster than an employee. In theory, a business should be willing to pay for AI services up to the level of the human salary it replaces. In fact, we heard one analyst describe the potential revenue generated by the AI model market as benchmarked to global salaries. Let that sink in.

Nearer term, we expect financial markets to remain volatile as investors continue to assess the evolving impact of AI on individual firm prospects and the economy more broadly. There will likely be a cycle here that mirrors that of earlier technological innovations, be it mobile communications or electric vehicles: early excitement draws capital into the sector, which inflates valuations, which then collapse once expectations become more realistic and the real winners emerge. As this process plays out, it is important to keep in mind just how much we don’t know about AI’s future. Until the landscape becomes clearer, we are maintaining a balanced exposure to AI across our portfolios, favoring companies with diverse business models, strong balance sheets, and leading market share positions. And we are keeping a careful eye on what we are willing to pay for growth.

Endnotes

1 “The AI investment landscape evolves”,

https://hansondoremus.com/ the-ai-investment-

landscape-evolves/

2 “How Many Businesses Are Using AI?”,

Economic Innovation Group

3 Real-Time Population Survey (Bick, Blandin,

and Deming, 2026), https://www.genaiadoptiontracker.

com/

4 “Everywhere but the Statistics,” The Economist,

February 28th issue, pages 62-64